Analyst Insight

Expect Mixed Trend, Ahead Of Weak Q2 Earnings Reports, June Economic Data

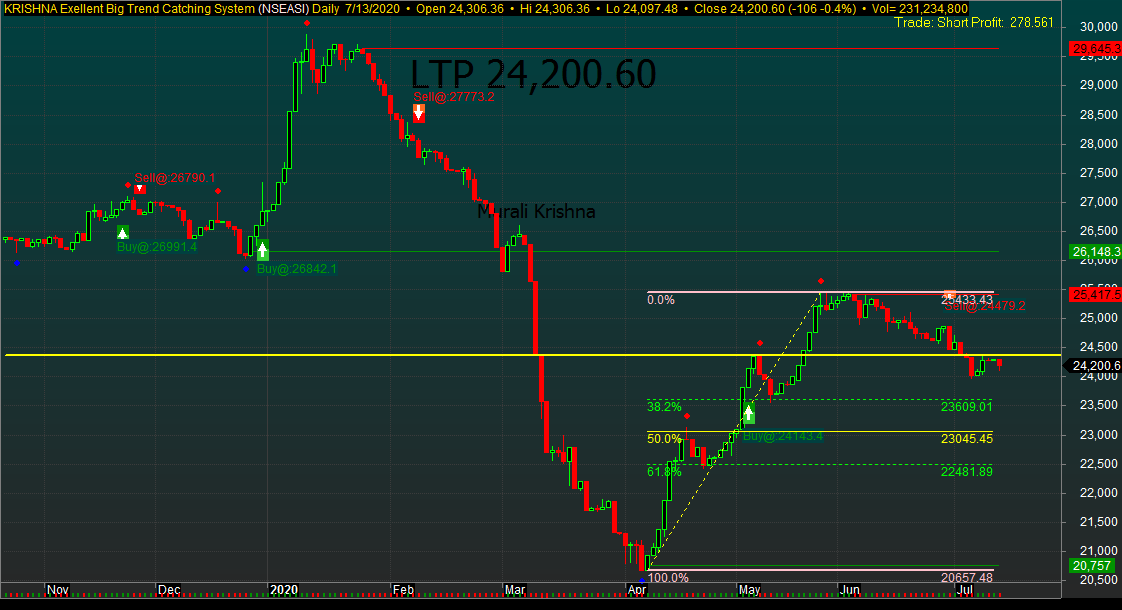

Market Update for July 13

Trading activities, Monday, continued on the Nigerian Stock Exchange (NSE), extending the negative outlook of last week by wiping out Friday’s marginal gains as profit taking hit banking stocks, made worse by selloffs in the high cap equities.

It was a mixed but high volatility session, especially as the composite NSE All-Share index traded below the 20 and 50-Day Moving Average on a very higher traded volume. The index closed lower on the first trading day of the week.

Just as discussed in our market update video before the market opened today, the banking sector’s exposure to the impact of the Coronavirus (COVID-19) pandemic, resulting in a downturn, especially to the energy sectors over the past five months.

According to available data, the energy sector accounted for 30% of loans and advances to the private sector. As of December 31, 2019, Nigerian banks disbursed a total of N18.63tr in loan to the real sector, with the oil and Gas sector accounting for all of N4.88tr, from N4.5tr, with the power sector alone owing N705.92bn.

The expectation of weak and mixed half-year scorecards in the midst of inconsistent government policies, and the rising new coronavirus cases have continued to trigger apathy for the stock market and the economy. This is regardless of government’s move to stimulate the economy through interventions in critical sectors, as contained in the N10.8tr revised budget signed into law by President Muhammadu Buhari last week.

Meanwhile, Monday’s trading opened in the downside, and was sustained throughout, despite oscillating in the late afternoon on buying interests in industrial and consumer goods stocks, while selloffs in banking and oil/gas stocks pushed the benchmark Index to an intra-day low of 24,097.48 basis points, from its high of 24,306.36bps and thereafter finished the session lower at 24,200.60bps.

Monday’s market technicals were negative and mixed as volume traded was higher than the previous session in the midst of breadth favoring the bears on mixed sentiments as revealed by Investdata’sDaily Sentiment Reportshowing a ‘sell’ position of 51% and buy volume of 49%. Total daily transaction volume index stood at 1.07, just as the impetus behind the day’s performance stayed weak, with Money Flow Index reading 35.85 points, down from the previous 36.71ps, indicating that funds left the market on continue selloffs.

Index and Market Caps

At the close of trading, the key performance index NSEASI shed 105.76 basis points, closing at 24,200.60bps, after opening at 24,306.36bps, representing a 0.44% decline, while market capitalization lost N55.17bn, closing at N12.62tr, from an opening value of N12.68tr, representing 0.44% depreciation.

If you are yet to sign up for Investdata’s Buy and Sell signal setup, don’t delay. We have just added another risk management feature and six categories of stocks to see you through in this changing market dynamics and economic uncertainties. These stocks are with double potentials to rally and protect your funds considering their current market prices.

To become a member, send ‘YES’ or ‘STOCKS’ to the phone numbers below. Take advantage of this service to buy right and sell right at this current market oscillation and earnings reporting season for portfolio realignment and positioning as we await an economic reform policy to stimulate and re-track the economy again.

The dowturn recorded was due to selloffs in MTNN, 11 Plc, Guaranty Trust Bank, Zenith Bank, Access Bank, UBA, ETI and Wapic Insurance which impacted negatively on the NSE’s benchmark index Year-To-Date loss position that increased to 9.84%, just as market capitalization YTD loss stood at N324.50bn, representing a 2.58% down from the year’s opening level.

Bearish Sector indices

All the sectorial performance indexes were down except for NSE Industrial goods index that closed higher by 0.26%, while NSE Oil/Gas indexes led the decliners after losing 1.91%, followed by NSE Banking that shed 1.70%, while the NSE Insurance closed 0.35% lower.

Market breadth was negative as decliners outnumbered advancers in the ratio of 17:14, while transactions in volume and value terms were up by 75.67% and 139.55% respectively, after investors exchanged 231.23m shares worth N2.15bn, from the previous day’s 131.63m units valued at N899.48m. Volume was boosted by trades in Sterling Bank, FCMB, Fidelity Bank, Guaranty Trust Bank and MTNN.

NPF Microfinance and Neimeth Pharm were the best performing, as they gained 10% and 9.35% respectively, closing at N1.32 and N1.52per share on low price attraction and market forces. On the flip side, 11 Plc and Chams lost 9.97% and 8.33%, closing at N173.40 and N0.22 per share respectively on selloffs.

Market Outlook

We expect the mixed trend to continue as earnings season kicks off any moment from now ahead of June inflation report and wobbling economic fundamentals, while inconsistent government policies continue to dampen investor confidence ahead of the expectedly disappointing half-year corporate earnings reports. This is likely to support the wave of decline as pullbacks persist, creating new entering opportunities. Money flow index has continued to look down at 35.85, despite flowing from one sector to the other, seeking value in terms of low prices with high upside potentials.

This is just as economic recovery is threatened by the rising cases of the COVID-19, ahead of the Q2 earnings reports season, which implies that opportunities are still available assectoral rotation continues. Also, sectors that have suffered oversold, so far, offer attractive risk-reward buy-opportunities and outlook for considerable short, medium and long term investment.

For immediate liquidity or cash let us trade low priced stocks with serious caution to avoid being trapped. However, the market’s high dividend yield continues to attract buying interests, as few audited and unaudited corporate earnings will hit the market, going forward. This is despite the likely continuation of selloffs. Investors are buying to increase their positions in undervalued stocks ahead of Q2 numbers. It is also against the backdrop of the fact that the capital wave in the financial markets may persist in the midst of relatively low-interest rates in the money market, high inflation, and unstable economic outlook for 2020.

Again, the current undervalued state of the market offers opportunities to position for the short, medium and long-term, which is why investors should target fundamentally sound, and dividend-paying stocks for possible capital appreciation going forward. Also, traders and investors need to change their strategies, because of the NSE’s pricing methodology, the CBN directives, and their impact on the economy in the nearest future.

Ambrose Omordion, Chief Research Officer, Investdata Consulting Limited